DASHBOARD: Digital infrastructure valuation comps for February 2026

- Publisher : Venture Insights

- Publish Date : March 5, 2026

This Digital Infrastructure Valuation report provides a comprehensive analysis of key financial metrics for digital infrastructure stocks listed in Australia, New Zealand, and the broader regional market. It includes detailed visualisations of monthly and annual share price movements, key earnings multiples, and forward earnings multiples compared to forward growth estimates. Additionally, it tracks share price trends over the past twelve months, offering valuable insights for market participants.

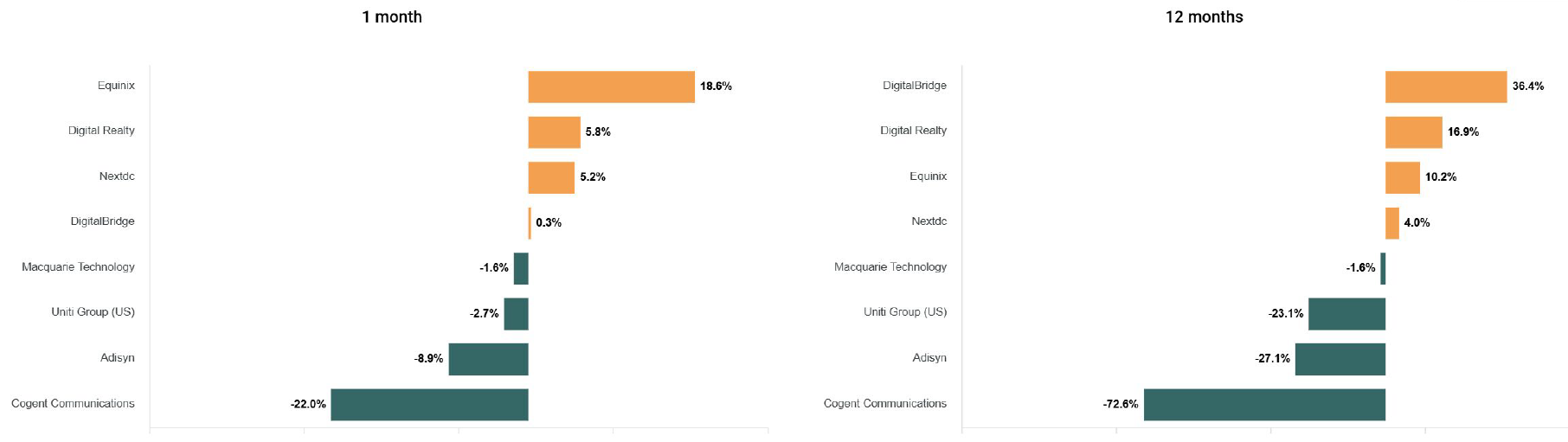

Figure 1: Digital infrastructure share price changes January 2026

Source: Firehawk. Only includes top 10 movers.

Key developments

Overall, listed digital infrastructure stocks in the region did well in 2024 as demand for AI infrastructure saw growing interest in the sector. Over 2025, a gradual investor turn against tech stocks and “AI hype” has weighed on stock prices.

Cogent Communications

Cogent Communications’ stock declined by 22% during February, after the company released its Q4 2025 and Full Year 2025 Results. Cogent’s full-year 2025 service revenue fell to US$975.8m from US$1,036.1m in 2024, reflecting strategic shifts following the Sprint acquisition. Despite this top-line contraction, the company achieved a 100.3% surge in wavelength revenue and a 43.8% increase in IPv4 leasing income. While operational efficiencies improved adjusted EBITDA margins, annual net cash used in operating activities widened slightly to US$10.6m compared to the previous year.

Equinix

Equinix’s stock jumped around 19% during the month, after the company released its Q4 2025 and Full Year 2025 Results and acquisition news. Equinix closed 2025 with US$9.217b in revenue, reflecting 6% normalised growth driven by record demand for AI and cloud infrastructure. Annual operating income surged 39% to US$1.848b, while adjusted EBITDA margins reached a robust 49%. Strategically, Equinix expanded its Nordic footprint through a US$4b joint acquisition with Canada Pension Plan Investment Board (CPP) of atNorth, adding high-density, liquid-cooled capacity to support high-performance computing workloads. Equinix will own a 40% stake with CPP owning the remaining 60% controlling interest.

NextDC

NextDC’S stock rose by around 6% during February, after the company released its 1HFY26 results. The company delivered record 1H26 results, with net revenue rising 13% to $189.2m and underlying EBITDA increasing 9% to $115.3m. Contracted utilisation surged 137% to 416.6MW, supported by a massive 296.8MW forward order book. Consequently, NEXTDC upgraded its FY26 capital expenditure guidance to $2.4–$2.7b to accelerate capacity expansion, while maintaining net revenue ($390-400m) and EBITDA targets ($230-240m)

Figure 2: Digital infrastructure valuation multiples

Source: Firehawk. Blank results are due to a lack of equity research analyst coverage, the EV/Revenue multiple being above 25x, or the EV/EBITDA and EV/EBIT multiple being less than zero or above 60x.

About Venture Insights

Venture Insights is an independent company providing research services to companies across the media, telco and tech sectors in Australia and New Zealand.