DASHBOARD: Media valuation comps for November 2025

- Publisher : Venture Insights

- Publish Date : December 10, 2025

This Media Valuation Comps report provides a comprehensive analysis of key financial metrics for media stocks listed in Australia and New Zealand (ANZ). It includes detailed visualisations of monthly and annual share price movements, key earnings multiples, and forward earnings multiples compared to forward growth estimates. Additionally, it tracks share price trends over the past twelve months, offering valuable insights for market participants.

Figure 1: ANZ media share price changes November 2025

Source: Firehawk. Only includes top 10 movers.

Key developments

Overall, the media sector in Australia and New Zealand struggled to maintain their positions over 2024 with the deterioration of economic conditions. 2025 promised relief, but unexpected softness in the advertising market has depressed share prices.

ARN Media

ARN Media’s stock declined by around 16% after the company issued a trading update highlighting significant softness in the Australian advertising market in 2H25, with October year-to-date revenue down ~10% and second-half revenue expected to fall by low double digits versus pcp. A $40m three-year cost-out program, of which $35m is actioned, is forecast to reduce H2 costs by ~8%, yet FY25 EBITDA is expected to be 25–27% lower as ARN pursues a broader entertainment-led growth strategy.

oOh!media

oOh!media’s stock fell by around 7% in the month after the company released a trading update during the month Q3 revenue grew 7% versus pcp, slightly ahead of prior guidance, with improved market share ex-Retail and New Zealand. A soft October advertising market and the non-renewal of the Auckland Transport contract are expected to leave Q4 revenue slightly below pcp and CY25 revenue at $689–694m, at ~43% gross margin. Operating costs of $159–161m and capex near the low end of $53–63m support CY25 Adjusted EBITDA guidance of $139–142m, with management highlighting disciplined cost control and execution.

Nine

Nine’s stock fell by 6% during November after the company provided a trading update flagging continued mid-teens (%) digital subscription growth at Nine Publishing, and reaffirming FY26 EBITDA growth at Stan underpinned by the new Premier League rights. Total TV advertising conditions remain softer than expected, with September–October revenues down mid–high single digits and visibility into Christmas still short. However, FY26 Total TV costs are now expected to decline mid-single digits, supporting H1 FY26 EBITDA growth and delivering >$100m of underlying cost out across FY26–27, ahead of prior guidance.

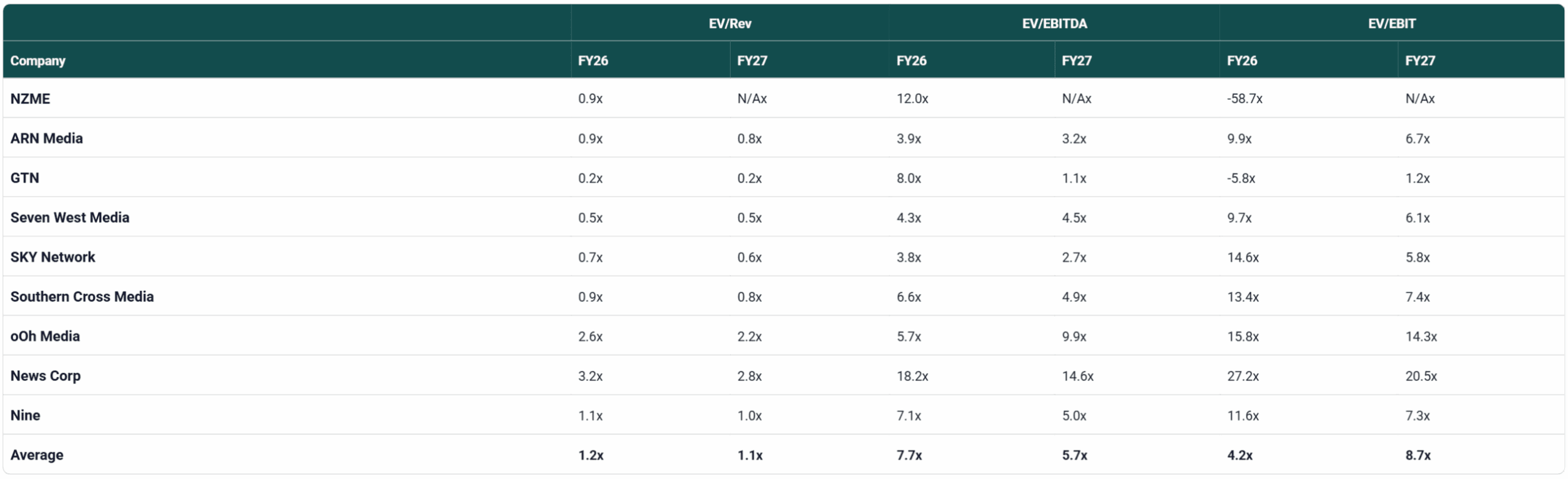

Figure 2: ANZ media valuation multiples

![]()

Source: Firehawk

About Venture Insights

Venture Insights is an independent company providing research services to companies across the media, telco and tech sectors in Australia, New Zealand, and Europe.